Accounting Competency Framework

Most accounting teams have job descriptions. Very few have a competency framework. The difference matters more than it sounds. A job description tells people what to do. An accounting competency framework defines what good performance actually looks like at each level, and it gives the organisation something to assess, develop and make decisions with.

What Is an Accounting Competency Framework?

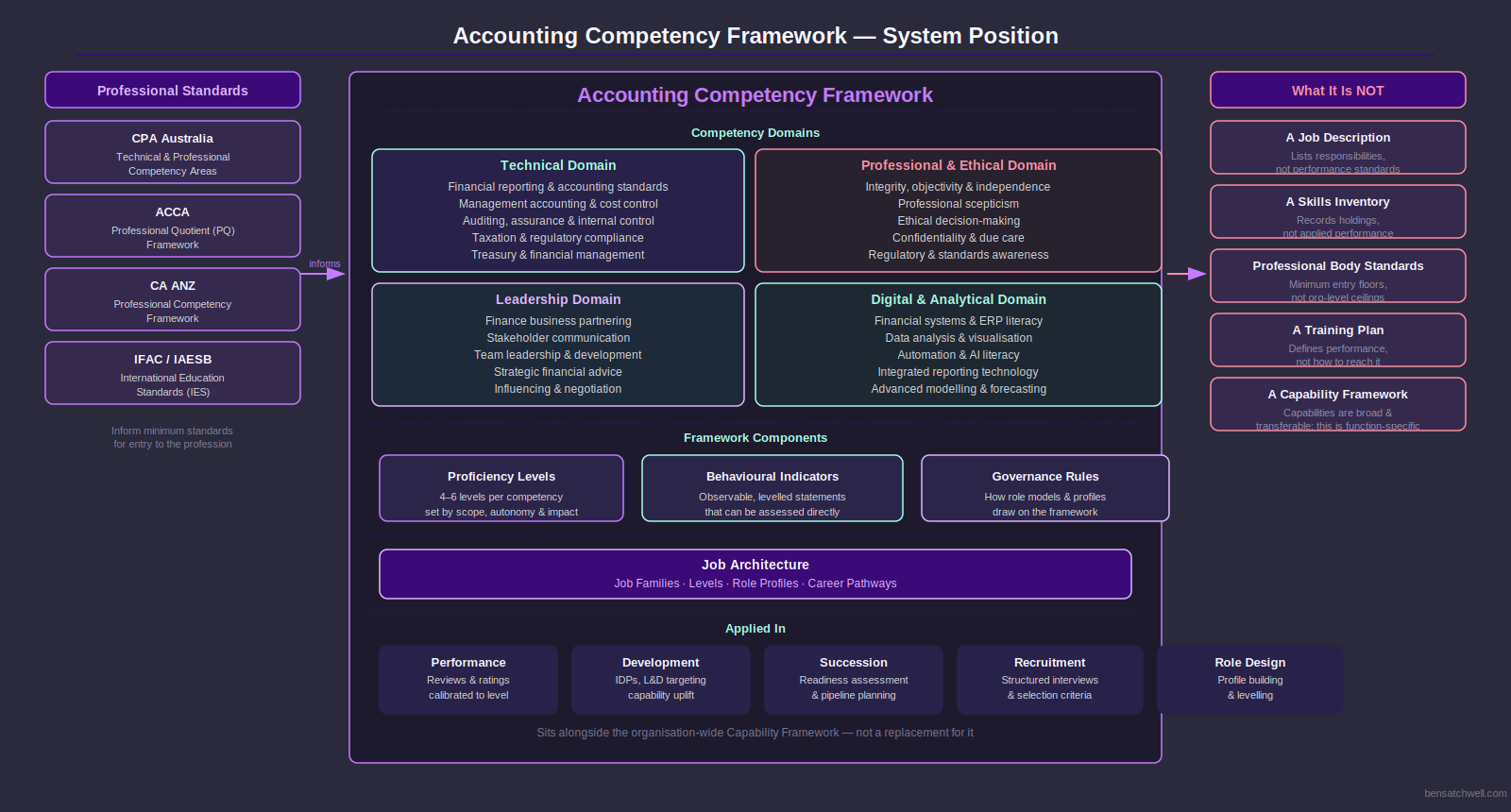

An accounting competency framework is an organisation-wide structure that defines the competencies required to perform effectively across accounting and finance roles, at each level of seniority and specialisation. It integrates technical knowledge, professional judgement, regulatory understanding and behavioural performance into observable, assessable standards.

Unlike a skills inventory or a professional development curriculum, a competency framework sets out what the integration of those skills looks like in practice. CPA Australia's professional accreditation guidelines distinguish between technical competency areas such as financial accounting and reporting, and enabling competencies such as professional and ethical behaviour, specifically because competence in accounting is never purely technical.

Why an Accounting Competency Framework Exists

Accounting functions suffer a specific and common problem: technical skill does not equal effective performance. A team member can pass professional examinations and still be unable to communicate financial findings clearly, manage risk appropriately under pressure, or exercise sound judgement in ambiguous situations.

Professional bodies have long recognised this. The International Federation of Accountants (IFAC) publishes an illustrative competency framework for accounting technicians that separates technical competencies from professional skills, and explicitly includes ethics, communication and problem-solving as core components of professional competence.

Without a framework, managers rely on experience and intuition to assess who is performing well and who is not. That produces inconsistency, bias risk and an inability to build structured development pathways. A competency framework gives the function a shared language for performance that everyone can use.

How an Accounting Competency Framework Works in Practice

A well-designed accounting competency framework is built from a defined set of competency domains, each containing individual competencies with proficiency levels and observable behavioural indicators.

Each competency carries proficiency levels, typically four to six, that describe what the competency looks like at Foundation, Practitioner, Advanced and Expert stages. These are not seniority labels. They are descriptions of the scope, autonomy and complexity at which someone performs.

Behavioural indicators are the practical unit of the framework. They describe observable acts in context, not personality traits or dispositions. "Prepares management accounts that clearly explain material variances and their business implications, without being asked" is a behavioural indicator. "Good communicator" is not.

Common Failure Modes in Accounting Competency Frameworks

Most accounting competency frameworks fail in one of three ways.

The first is technical overload. The framework becomes a taxonomy of accounting standards, software skills and regulatory knowledge, with almost no attention to behavioural performance, professional ethics or judgement. The result is a framework that tells you what people know, not how they perform.

The second is behavioural vagueness. Competencies are defined with language so abstract that nobody can assess them meaningfully. "Demonstrates integrity" appears in half the frameworks in circulation. It is not useful. Integrity at what level, in what context, observable how?

The third is disconnection from professional standards. CPA Australia, ACCA, ICAEW and CPA Canada have each developed detailed competency frameworks anchored in professional standards. An internal framework that ignores these bodies and their definitions invents language for things that already have rigorous definitions. This is avoidable effort that produces inferior results.

Organisations with well-functioning HR competency frameworks understand this trap intuitively. The same logic applies in finance functions.

Named Frameworks and Standards

Several professional bodies have published accounting competency frameworks that organisations can draw from or align to.

CPA Australia publishes detailed technical and professional competency areas as part of its professional accreditation guidelines. These distinguish between technical competency areas, including financial accounting and reporting, management accounting, and strategic management, and enabling competencies including professional and ethical behaviour and communication.

ACCA publishes a competency framework structured around three performance objectives: professionalism, ethics and governance; stakeholder relationship management; and strategy, innovation and performance. Each is supported by observable performance outcomes against which members are assessed.

IFAC through the IAESB publishes an illustrative competency framework for accounting technicians that separates technical competencies from professional and enabling skills, and can serve as a reference structure for organisational design.

An internal accounting competency framework that borrows structure and definitions from these bodies is more defensible, more aligned to professional registration requirements, and more credible to practitioners than one built in isolation.

Trade-offs and Constraints

Not every organisation needs a fully bespoke accounting competency framework. For smaller finance teams, aligning to a professional body framework such as ACCA's or CPA Australia's competency structure may be sufficient as a starting point, with minor contextual adaptation.

For larger organisations, particularly those in financial services, public sector, or listed entities with significant reporting obligations, a tailored framework that maps to the organisation's specific role architecture and risk environment is worth the design investment. A CFO competency framework, for instance, will look quite different from the framework for a transactional processing team, and both should draw on but extend beyond the generic accounting standards.

The single constraint that applies universally: an accounting competency framework is only as useful as the processes it connects to. If it does not inform performance conversations, development planning and promotion decisions, it is documentation for its own sake.

A technical competency framework for accounting must therefore be embedded in the people cycle, not produced as a standalone artefact and filed.

Frequently Asked Questions

What is included in an accounting competency framework?

An accounting competency framework typically includes competency domains covering technical accounting, financial analysis, risk management, professional ethics, and communication. Each domain contains individual competencies defined at multiple proficiency levels, with behavioural indicators describing observable performance at each level.

How is an accounting competency framework different from a job description?

A job description outlines the tasks and responsibilities of a role. A competency framework defines what effective performance in those tasks looks like, at different levels of proficiency. You can use a competency framework to assess, develop and compare people. A job description does not give you that capability.

Should an accounting competency framework reference professional body standards?

Yes. CPA Australia, ACCA, IFAC and ICAEW have all published detailed competency frameworks for the accounting profession. An internal framework should align to these rather than invent parallel definitions. This makes the framework more credible, more aligned to professional development pathways, and easier to maintain as standards evolve.

How many competencies should an accounting competency framework contain?

Workable frameworks typically contain six to twelve competencies grouped into three to five domains. Frameworks with more than fifteen competencies become difficult to assess against and are rarely used meaningfully in practice.

Can the same competency framework apply across all accounting roles?

The framework defines the domain. Competency models apply a selection of competencies from the framework to specific roles or levels. A graduate accountant and a financial controller draw on the same framework but with different competency selections and different proficiency expectations.

What proficiency levels should an accounting competency framework use?

Most accounting frameworks use four to six levels, typically labelled Foundation, Practitioner, Advanced and Expert, and in some cases Distinguished. Levels are defined by scope, autonomy and complexity, not by years of experience or job title.